If you're overwhelmed with debt, there's still hope. Our automated software will help you resolve your debt and move forward.

How to Settle a Debt in Delaware

Summary: Getting sued for debt is not fun. Luckily, you can work out a debt settlement plan at any stage of the lawsuit process in Delaware. Just be sure to respond to the case before the 15-day deadline, send a settlement offer to kickstart negotiations, and get the agreement in writing. SoloSettle can help you with all of these steps and more.

If you’re like most American adults and have a few credit cards, an auto loan, or a mortgage, you know how important it is to manage your debts. Repaying your loans keeps you in good standing with your creditors and builds your credit score.

However, sometimes it’s impossible to keep making all of your payments. A job loss or other unexpected event can result in lost income and make you fall behind.

Whatever the reason for your stopped payments, creditors will take action. They’ll call you or send you letters. They may charge off your account and sell it to a debt collector. Sometimes, they even take legal action against you.

When a creditor decides to sue you for unpaid debt, they’ll seek a judgment from your local court. A judgment grants your creditor additional rights to collect on the obligation. They’ll be able to garnish your wages or freeze your bank account. If your property is collateral for a loan, they might seize it.

Luckily, there are ways to avoid a judgment and the hassle that it creates. One way is through debt settlement.

In this article, we’ll discuss how to settle a debt in Delaware, including state-specific laws and requirements.

There are 3 main steps to debt settlement

If you’ve been sued for debt in Delaware, you can reach out to your creditor or debt collectors at any stage of the process to settle your debts. Follow these three steps to settle your debt in Delaware:

- Respond to the debt lawsuit with an Answer.

- Make an offer to start negotiations.

- Get the settlement agreement in writing.

Now, let’s take a closer look at each of these steps. Don’t like reading? Check out this video instead:

1. Respond to the debt lawsuit with an Answer

A lawsuit begins when your creditor or a debt collector files a Complaint against you in your local Delaware court. A Complaint indicates the reasons for the case, such as nonpayment of your obligation. It will stipulate the amount of money you owe, including interest and fees.

You have 15 days to respond to a debt lawsuit in Delaware. To respond, you must reply to each claim listed against you in the Complaint. If you don’t respond in time, there is a good chance you will lose automatically when a default judgment is entered against you.

Even though you plan to settle your debt before your court date, you should still file a response to the lawsuit. A legal response is known as an Answer. In your Answer, you’ll defend yourself against the claim.

There are several defenses people commonly use in their Answers. You might claim that the creditor hasn’t properly validated the debt or that the amount of the obligation due is incorrect.

Make the right defense the right way with SoloSuit.

2. Make an offer to start negotiations

Your next step is to figure out how much you can offer to settle the debt. Estimate how much money you have in savings and how much you expect to earn in the next few weeks. If you don’t have much cash, consider taking on an odd job or asking friends and family for help.

We recommend that you offer around 60% of the total value of your debt. That amount is enough for creditors and debt collectors to know you genuinely want to resolve the obligation. They’ll consider whether a lump-sum payment from you is better than going through a lengthy collection process that isn’t certain to deliver results.

If there is no way you can afford 60% of the debt, offer what you can and explain your financial circumstances. Sometimes creditors are more willing to negotiate if they understand your situation. And since most debt collectors purchase old accounts at a small portion of the original debt amount, there is a good chance they’ll accept a lower offer too. Both creditors and collectors may be willing to accept less or offer alternative arrangements.

SoloSettle takes care of the negotiation process for you.

3. Get the settlement agreement in writing

Before sending your creditor any money, get an agreement in writing. Your written agreement ensures that both parties understand the contract terms.

It’s important to get everything in writing because debt collectors are known to make verbal agreements and go back on their word. For example, they might agree to accept a percentage of the debt to settle and then continue with the legal process when you don’t respond in court.

A written agreement will protect you from sketchy debt collector activity.

Your contract should indicate how much you’ll repay the creditor, when your payment is due, and how you’ll transfer the funds. It should also stipulate that your payment fully settles the debt and that your creditor releases their rights to the remaining amount.

We recommend you include a space for a notary to witness the agreement signing for you and your creditor. A notary’s signature adds an additional layer of protection to the contract.

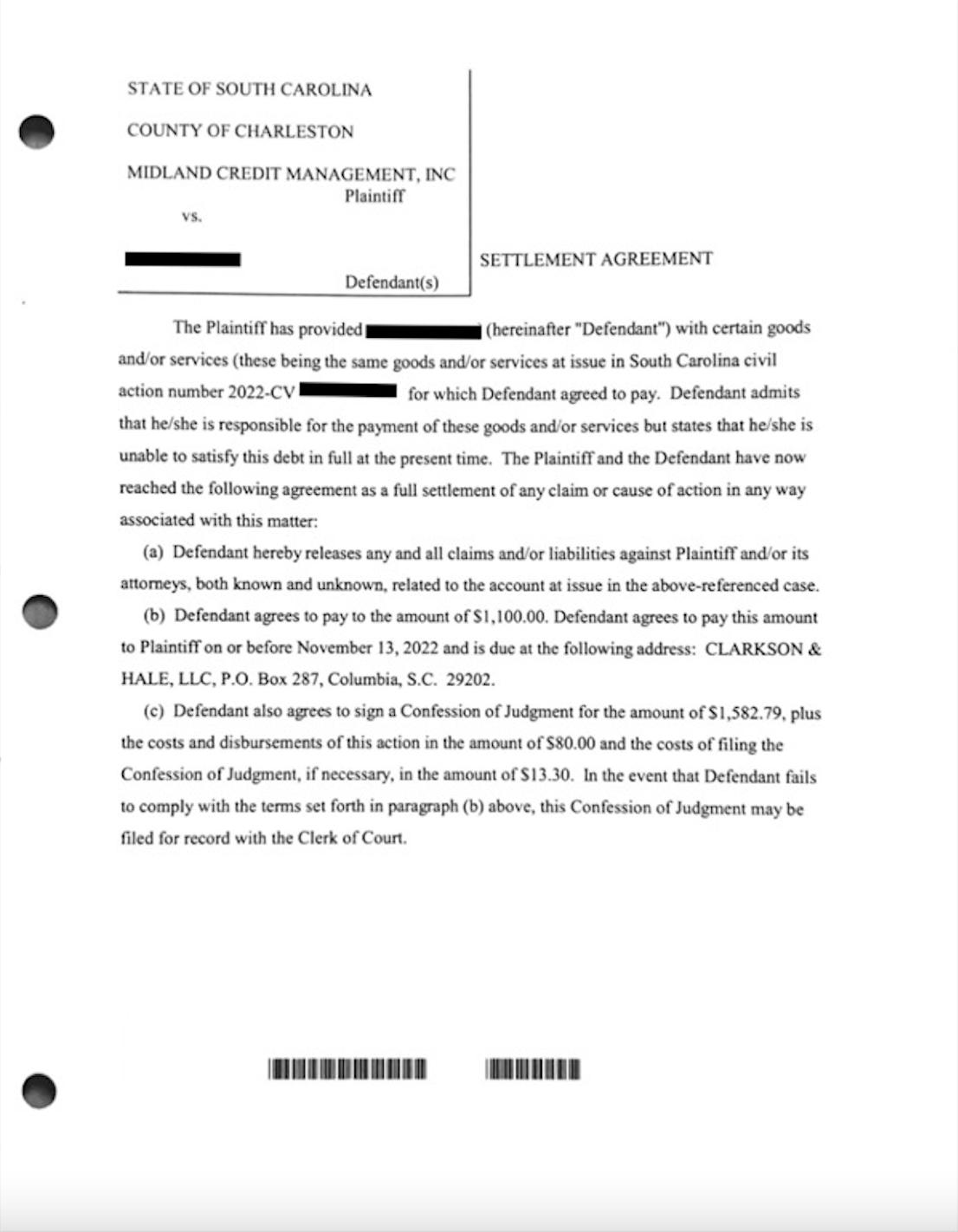

Here is debt settlement agreement example, with a preview attached below, to give you an idea of what should be included in yours:

Now that we’ve reviewed the debt settlement process, let’s consider a hypothetical example.

Example: Clara lives in Delaware, and she receives a Summons and Complaint from Encore Capital Group, notifying her of a lawsuit against her. Encore claims she owes $5,000 from an old credit card account that was charged off and transferred to them. To protect her right, Clara uses SoloSuit to respond to the lawsuit before Delaware’s 15-day deadline. This buys her time to explore other options, like debt settlement. Next, she assesses how much she can repay to settle the debt once and for all. After taking a close look at her finances, Clara decides she can afford to pay up to 70% of the debt. She uses SoloSettle to send an initial offer, starting low at just 50% of the debt. After a few rounds of negotiations, Encore Capital Group agrees to settle the debt at 65%, or $3,250. Encore drops the case against Clara and reports the account settled to the credit reporting bureaus.

What are Delaware’s debt settlement and debt collection laws?

Delaware’s Debt Management Services Act keeps debt settlement companies accountable. It prohibits certain actions by and regulates the licensure of such agencies. According to the Debt Management Services Act, debt settlement companies cannot:

- Take a consumer’s money and use it in any other way than to hold it in a trust and eventually settle a debt.

- Settle a debt on behalf of a consumer for more than 50 percent of the amount of the debt owed to a creditor, unless agreed upon by both the consumer and creditor.

- Claim that payment of a certain amount will settle a certain amount or range of indebtedness.

- Claim that enrolling in their program will prevent litigation, garnishment, attachment, repossession, foreclosure, eviction, or loss of employment.

- Pretend they are equipped to provide legal advice or services.

Delaware also adheres to the Fair Debt Collection Practices Act (FDCPA). The FDCPA prevents debt collectors and creditors from taking specific actions against a consumer, including the following:

- Calling a debtor before 8 a.m. or after 9 p.m.

- Telling a consumer they’ll go to jail for failing to repay their debts.

- Contacting a debtor at work if the debtor asks them not to.

- Publishing the debtor’s obligation in any type of public forum.

- Pretending to be someone else when contacting the consumer.

- Threatening to destroy the consumer’s reputation if they don’t repay a debt.

Delaware has a statute of limitations for debt collection. Under 10 DE Code § 8106 (2012 through 146th Gen Ass), written and oral contracts have a statute of limitations of three years, as does a collection on account.

What’s the best debt settlement company?

If you’re ready to try debt settlement, you can contact one of these companies for help.

SoloSettle

SoloSettle is the best solution for anyone facing a current debt lawsuit. Before your court date, SoloSettle handles the debt settlement negotiation process for you.

We’ll negotiate a settlement on your behalf. Once you agree to it, we’ll make sure you have a written contract. Then, we’ll deal with the payment process, so you won’t need to worry about handing over your banking information to a debt collector.

SoloSettle is different from other debt settlement companies for several reasons:

- SoloSettle can help you settle a debt of any size, whereas many debt settlement companies require you to have a debt over $15k.

- SoloSettle actively attempts to settle your debt, whereas many debt settlement companies take a more passive role, waiting for settlement offers to come to them.

- SoloSettle has legal defense built in with SoloSuit. While settling, you can use SoloSuit to block lawsuits if you need. Most debt settlement companies don’t provide legal defense; if you’re sued for a debt you are on your own.

- SoloSettle is offered by SoloSuit, a trusted brand and a legitimate company. Many traditional debt settlement companies are actual scams.

National Debt Relief

National Debt Relief is a debt settlement company that helps consumers settle their unsecured debts. The company has a strong track record of successful results and can help reduce obligations by 50% or more in a settlement. To enroll in the program, you must have at least $7,500 in debt and agree to a monthly repayment schedule.

Freedom Debt Relief

Freedom Debt Relief is another large and well-known debt settlement company. Since 2002, the company has helped over 650,000 people eliminate their obligations through debt settlement. Programs last two to four years, and the company charges 15% to 25% of the client’s debt for its services.

Accredited Debt Relief

Accredited Debt Relief is a debt settlement company known for its customized debt relief options. Consumers who enroll in its programs make monthly payments, which Accredited Debt Relief uses to resolve their outstanding obligations. You will pay 15% to 25% of your debt for its services.

What’s the best way to contact my creditor?

If you’re ready to settle your debts, you’ll need to contact your creditor or debt collector. You can reach out to them via email, phone, or letter.

In our opinion, email is the best way to start the settlement process. Email provides you with a written record of the conversation. You’ll be able to refer to it if you need to later. You’ll also have time to consider your creditor’s messages before responding.

Calling is appropriate if you’re short on time or prefer to speak with your creditor. We recommend recording your conversation. That way, you have a record of what was said during the phone call.

Under Delaware law 11 DE Code § 2402, both parties must consent to record a phone call; you'll need to get permission from your creditor before starting to record.

FAQs on how to settle a debt in Delaware

You may have other inquiries concerning debt settlement in Delaware. Here are a few of the most common questions we hear.

Q. At what point does a debt become uncollectible in Delaware?

Debts have a statute of limitations of three years in Delaware. After that, the debt becomes time-barred, and creditors can no longer pursue a lawsuit against you. However, they can report your account negatively to credit reporting bureaus, send you letters, and call you.

Q. What percentage of debt should I offer to settle?

We recommend that you offer at least 60% of the value of your debt in a settlement. That’s typically enough to attract your creditor’s attention and encourage them to negotiate with you. If you can’t afford 60% of your debt’s value, offer what you can and explain your financial circumstances.

Q. Can I do my own debt settlement?

Yes, you can handle debt settlement yourself — and it will save you money on the fees charged by debt settlement organizations. However, you should understand the process before contacting your creditors.

How to get debt relief in Delaware

SoloSuit has several guides concerning debt relief and debt collections in Delaware. Here are a few you can review:

- Delaware Statute of Limitations on Debt | SoloSuit Blog

- How to Answer a Summons for Debt Collection in Delaware (2020 Guide) | SoloSuit Blog

- Delaware Court Case Search — Find Your Lawsuit | SoloSuit Blog

You don’t have to accept a judgment — debt settlement is possible

Facing a debt lawsuit is anxiety-inducing, but you can settle the matter before your court date. Make sure to learn about how the process works before starting. Once you figure out how much you can offer in a debt settlement, speak with your creditor and get the agreement in writing. Then, you can transfer the money and move on from the debt.

Check out SoloSuit’s solutions for debt settlement today.

What is Solo?

Solo makes it easy to resolve debt with debt collectors.

You can use SoloSuit to respond to a debt lawsuit, to send letters to collectors, and even to settle a debt. SoloSuit's Answer service is a step-by-step web-app that asks you all the necessary questions to complete your Answer. Upon completion, we'll have an attorney review your document and we'll file it for you.

SoloSettle can help you contact your debt collector or creditor and negotiate the debt to settle for less, all online. It simplifies and streamlines the process to settling your debt.

No matter where you find yourself in the debt collection process, Solo is here to help you resolve your debt.

>>Read the NPR story on SoloSuit. (We can help you in all 50 states.)